Tax Cuts and Jobs Act Makes Immediate and Long-Term Modifications to Complex IRS Rule

Tax Cuts and Jobs Act Makes Immediate and Long-Term Modifications to Complex IRS Rule

Tax Cuts and Jobs Act Makes Immediate and Long-Term Modifications to Complex IRS Rule

Tax Cuts and Jobs Act Makes Immediate and Long-Term Modifications to Complex IRS RuleAs we’ve been saying since the Tax Cuts and Jobs Act was passed by Congress and signed into law by President Trump last December, it’s taking a while to unpack and analyze this massive tax reform document.

One of the changes that is likely to have impact on your company’s income taxes is related to business meals and entertainment expenses. Some rules have stayed the same, some have changed, and some won’t take effect until 2025.

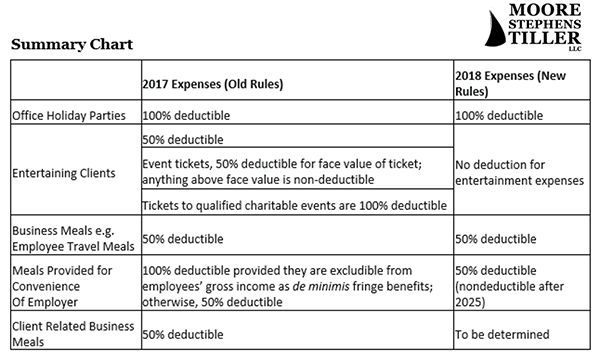

No Modifications

There will be no changes in the current regulations related to food and beverage expenses that are associated with the operation of your trade or business. The deduction for office holiday parties will remain the same, at 100 percent. When employees travel for work, you will still be able to deduct 50 percent of these meal expenses.

Some Deductions Lost

Your ability to claim expenses associated with entertaining clients, though, will be affected by the new tax law. You will no longer be allowed to deduct 100 percent of the cost of tickets to qualified charitable events. Nor will you be able to claim 50 percent of:

- Activities you undertake for entertainment, amusement, or recreation purposes, including sporting events, golf outings, etc.

- Dues that grant you membership to a club or organization that exists for the purposes of business or pleasure, recreation or socialization.

- Any facility that would be used to support any of these activities.

These new exclusions take effect for expenses incurred after December 31, 2017.

Expanded 50 Percent Limit

Also, as of December 31, 2017, the 50 percent meals and entertainment deduction was expanded to include expenses that are, “…associated with providing food and beverages to employees through an eating facility that meets requirements for de minimis fringes and for the convenience of the employer.”

Some Deductions Still Uncertain

The biggest potential impact may come from client-related business meals that are not associated with entertainment. It is still unclear as to how these types of expenses will be treated under the new tax reform. We will keep you posted as guidance and clarification is released by the IRS.

Planning Tip

One thing that you can do now is to set up a separate general ledger account for business entertainment and meal expenses that are nondeductible. You probably already have an account for 50 percent deductible and 100 percent deductible items. By coding items correctly now, you may be able to save some time at year end.

Ask for Clarification

The IRS looks closely at deductions claimed for business meals and entertainment expenses. At best, you might be questioned about them, and at worst, audited. We can help ensure that you’re complying with the agency’s changing rules in this area as well as many others. Contact us, and we’ll help you begin to plan for your 2018 taxes.