January 19th, 2021

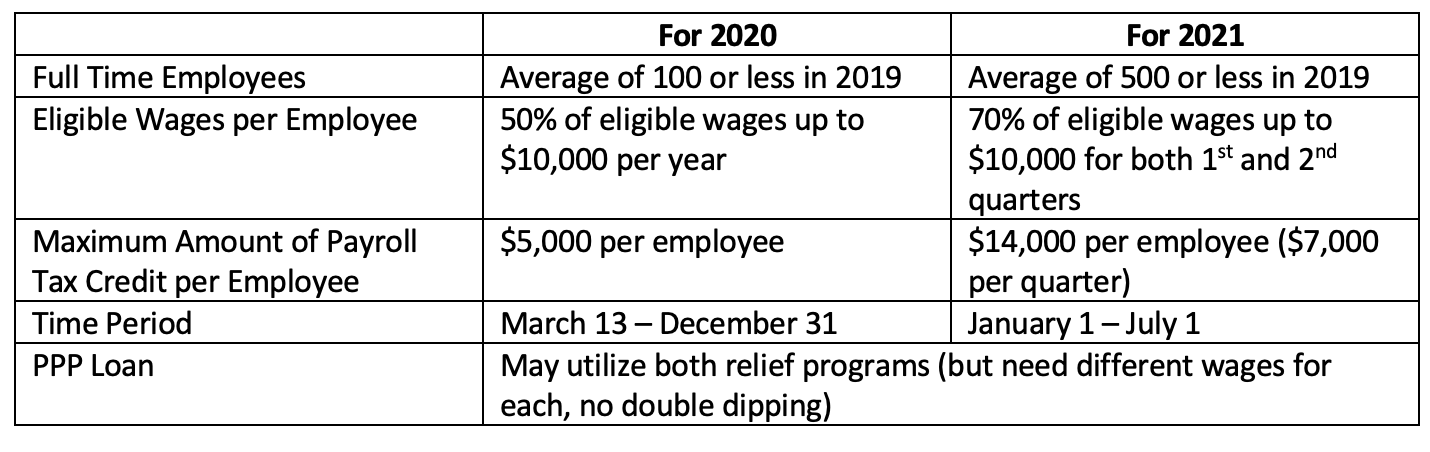

Could You Qualify for the Employee Retention Credit?

Did you know that the Consolidated Appropriations Act, signed into law in December 2020, enhanced and expanded the Employee Retention Credit program originally created in the 2020 CARES Act? The comparison in the changes can get confusing quickly, so let’s just focus on what is now available with the new law, instead of comparing the nuances of each!

Now to get this credit your Company either 1) had a government shutdown of some sort or 2) suffered a significant reduction of gross receipts. If you had a government shutdown of some sort, the credit is only available to you when you were shutdown. To meet the gross receipts reduction, there must be a 50% decline in gross receipts in a 2020 quarter compared to the same quarter in 2019. For 2021, the threshold decreases to be a 20% decline in gross receipts compared to the same quarter in 2019.

A few other specifics the new law includes are as follows:

These new provisions can be lucrative for employers who suffered hardships and continued to pay employee wages and healthcare expenses. This credit is instant cash relief against the employer’s 6.2% share of Social Security employment tax! There are some additional technical nuances related to the credits so please contact your MST professional if you think you may qualify for this credit or would like further details.

December 22nd, 2020

PPP Update | Changes in the Latest COVID-19 Stimulus Package

Congress has passed the Consolidated Appropriations Act 2021 which contains additional coronavirus aid for businesses and individuals. Now, the bill goes to President Trump to be signed into law. This update outlines key provisions within the legislation, focusing on significant changes to the Paycheck Protection Program (PPP). Here’s what you need to know.

PPP Expenses are Tax Deductible, Loan Forgiveness is Not Taxable

Business expenses paid with PPP loans are now tax deductible. This provision aligns with the congressional intent in the CARES Act and overturns the IRS Revenue Ruling from November 2020, which stated expenses were not tax deductible. For partnerships or S corporations, any amount excluded from income shall be treated as tax-exempt income. Additionally, tax basis and other attributes of the borrower’s assets will not be reduced. These provisions are retroactive to the date of enactment of the CARES Act (March 27, 2020).

There are more ways to use your PPP funds. Forgivable expenses now include:

- Operations expenditures – payments for any business software or cloud computing service that facilitates business operations, product or service delivery, the processing, payment or tracking of payroll expenses, human resources, sales and billing functions, or accounting or tracking of supplies, inventory, records, and expenses

- Property damage – costs related to property damage, vandalism, or looting due to public disturbances that occurred during 2020 that wasn’t covered by insurance or other compensation

- Supplier costs – payments made to a supplier for the supply of goods that are essential to the entity’s operations at the time the payment was made. The contract or purchase order must have been in effect before the loan’s covered period.

- Worker protections – operating or capital expenses made to comply with CDC, OSHA, Department of Health and Human Services’, or local or state requirements to maintain worker or customer safety related to COVID-19. Examples include the installation of drive-thru windows, air filtration systems, physical barriers such as sneeze guards, any health screening costs, and the expansion of additional indoor, outdoor, or combined business space.

The requirement to use 60% of the loan on payroll costs still applies.

Simplified forgiveness for PPP loans of $150,000 or less

The SBA must simplify the loan forgiveness process for borrowers who received PPP loans of $150,000 or less. The process should require borrowers to sign and submit a one-page certification form to their lender. The only information you’ll have to provide on this one-page form is:

- The number of employees you were able to retain because of the PPP loan

- The estimated amount of the loan you spent on payroll costs

- The total loan value

In addition, you must attest that you’ve accurately provided the required certification and complied with PPP loan requirements. After you submit the certification form, make sure to retain employment records for four years and other records for three years that prove your compliance. The SBA must create the certification form within 24 days of the Act’s passing.

Second draw loans for businesses facing severe revenue reductions

You can apply for a second PPP loan if you meet the following requirements:

- You employ no more than 300 employees

- You experienced at least a 25% reduction in gross receipts from one quarter in 2020 to the same quarter in 2019

The applicable quarters may change based on when you were in business. However, a 25% reduction in gross receipts from a quarter in 2020 compared to the same quarter in 2019 is a good rule of thumb.

If you apply for a PPP loan, your maximum loan amount will be 2.5 times your average monthly payroll costs in a year or $2 million. The maximum loan amount for NAICS 72 entities is 3.5 times your average monthly payroll costs in a year or $2 million.

Request an increase to your loan amount

If you applied for a loan but didn’t accept the full amount, you may ask to increase your loan amount to the maximum amount applicable. You can make this request even if you’ve received the initial loan amount or your lender has submitted a Form 1502 report to the SBA.

Select your covered period

Borrowers can select the end date of their covered period. It should fall between 8 and 24 weeks after the loan origination date.

Expanded eligibility

Certain 501(c)(6) organizations and destination marketing organizations that have 300 employees or fewer can now apply for a PPP loan. This includes chambers of commerce, economic development organizations, and tourism offices. News organizations and housing cooperatives can also apply for a PPP loan. Original program requirements and rules apply.

Generally speaking, lobbying organizations and organizations that spend more than 15% of its activities on lobbying efforts aren’t eligible for a loan. This bill prohibits recipients from using loan funds for lobbying activities.

Farmers & ranchers

There’s a new method for calculating your PPP loan if you’re a farmer or rancher. You can take your 2019 Schedule F gross income (capped at $100,000), divide it by 12, then multiply it by 2.5. Again, your maximum loan amount is limited to $2 million. If you received a PPP loan before this Act, you can ask your lender to recalculate your loan amount based on this formula. If this increases your loan amount, your lender can provide you with the difference.

Again, President Trump must sign this bill for it to become law. We’ll continue to update you as we learn more about the bill and any related guidance. As always, please reach out to us if you have any questions.

November 20th, 2020

An Important Update That Will Likely Have A Significant Impact On 2020 Taxes For PPP Recipients

The IRS issued guidance yesterday (Revenue Ruling 2020-27) regarding the deductibility of expenses that are paid with PPP loan proceeds (salaries, rents, etc.). The news is not encouraging. As you will remember, the PPP program was initially offered with the understanding that the proceeds would be tax free to the extent they were used for qualifying expenses. The IRS later ruled that while the proceeds could be tax free, taxpayers would not be able to deduct the expenses paid using the proceeds, essentially making the proceeds taxable. There has been a lot of noise about Congress legislating a change that would make the proceeds deductible – but so far no action on that front.

Yesterday’s IRS guidance states that the qualifying expenses will not be deductible in the year in which they are paid/incurred (ie 2020) regardless of when the taxpayer applies for forgiveness. Consequently, 2020 tax planning should factor in this lost deduction, and taxpayers will keep their fingers crossed for Congressional action.

One tiny silver lining to consider – assuming the deduction is in fact lost for 2020, it is better to lose it in 2020 at the existing lower tax rates vs losing the deduction in 2021 and paying the tax at an expected higher rate (assuming a tax rate increase is enacted for next year). Something to keep an eye on.

Please contact your MST professional if you would like further details.

April 9th, 2020

Non-profit Tax Deadline Relief

The IRS issued Notice 2020-23 on April 9, 2020 which provides filing and payment deadline relief for many returns required for non-profits and other tax exempt organizations. For non-profits and private foundations, this primarily impacts the returns and payments that would otherwise be due on May 15, 2020. Generally speaking, all May 15, 2020 federal filing and payment deadlines for Form 990-PF, and 990-T have been delayed to July 15, 2020. No filing or notification to the IRS on May 15 is necessary to obtain the deadline relief – it is automatic.

CAUTION – this Notice does not appear to provide filing deadline relief for calendar year end Form 990’s which would otherwise be due on May 15, 2020. This could be an oversight or may be intentional. We will await further guidance from the IRS on this matter. For now, we would recommend the filing of an extension on May 15, 2020 for calendar year Form 990’s (pending additional guidance).

We would anticipate that most states would follow along with this relief, but we will monitor that and provide information as it becomes available.

April 9th, 2020

IRS Offers Additional Relief and Guidance

The IRS Offers Additional Relief and Guidance published additional relief and guidance on upcoming key tax deadlines for individuals and businesses.

Last month, the IRS announced that taxpayers generally have until July 15, 2020, to file and pay federal income taxes originally due on April 15. No late-filing penalty, late-payment penalty or interest will be due.

Today’s notice expands this relief to additional returns, tax payments and other actions. As a result, the extensions generally now apply to all taxpayers that have a filing or payment deadline falling on or after April 1, 2020, and before July 15, 2020. Individuals, trusts, estates, corporations, non-profits, and other non-corporate tax filers qualify for the extra time. This means that anyone, including Americans who live and work abroad, can now wait until July 15 to file their 2019 federal income tax return and pay any tax due.

- Extensions past July 15. Taxpayers (and business) may file an extension to file by July 15, and those returns will be extended to October 15. However, this is only an extension to file, and not an extension to pay. Payments (or estimated with extensions) are still due by July 15 to avoid interest and penalties.

- Estimated Tax Payments. Besides the April 15 estimated tax payment previously extended, today’s notice also extends relief to estimated tax payments due June 15, 2020. This means that any individual or corporation that has a quarterly estimated tax payment due on or after April 1, 2020, and before July 15, 2020, can wait until July 15 to make that payment, without penalty.

April 7th, 2020 2:01PM

New FAQ on the PPP Program

Yesterday, the Small Business Administration (SBA) released additional guidance on the Paycheck Protection Program (PPP). Please click below to download a copy of this information.

Click here to download the FAQs for the Paycheck Protection Program

March 31st, 2020 5:20PM

Paycheck Protection Program Application

Please find LINKED BELOW the application for the Paycheck Protection Program (PPP), which is part of the recently signed CARES act.

Click here to download the PPP Application

March 30th, 2020 11:01AM

We want to get you the most relevant and up to date information on the Coronavirus Aid, Relief, and Economic Security (“CARES”) Act, signed Friday by President Trump, and other developments related to COVID-19. This email will provide highlights of the significant provisions impacting small businesses and their owners. A separate email will follow providing information on the provisions impacting individuals.

Paycheck Protection Program (PPP)

The PPP is perhaps the most significant part of the legislation impacting small businesses. This provides loans for business interruption resulting from COVID-19. These loans are interest bearing (not more than 4%) and non-recourse. It is expected that the application and approval process for these loans will be quicker and much less onerous than typical SBA loans.

Who’s eligible: Any business that employs less than 500 people; sole proprietors/independent contractors/self-employed persons; and accommodation and food service business concerns with multiple locations, but that employ not more than 500 persons per location. This eligibility includes for-profit businesses and non-profits.

The loans are designed to help borrowers cover payroll costs and other working capital expenses. Funds may be used to cover payroll (including commissions), and operating costs such as benefits, rent, mortgage, utilities, and interest on previously incurred debt.

The loans are eligible for forgiveness, but any unforgiven portion will be repayable over 10 years. This loan cannot be used in addition to the SBA Economic Injury Disaster Loan (EIDL) program.

Loan forgiveness – Loan principal amounts are eligible for forgiveness if during the 8 week period after the loan is disbursed the funds were used for eligible purposes – payroll, benefits, rent, etc. If the borrower reduces salaries or the number of employees (or both) during the 8 week period, a formula calculates a reduction for the amount forgiven. The loan forgiveness is not taxable to the borrower.

Maximum loan amount – Lesser of $10 million or 2.5 X average 2019 monthly payroll (excluding compensation above $100,000 per employee)

Important caveat – borrowers must make good faith certification that they need the funds to operate because of current economic disruption and will deploy funds for eligible uses. The details and requirements on this certification will be critical, keep an eye on this.

Where can you apply for the Paycheck Protection Program? Businesses can apply for the Paycheck Protection Program at any lending institution that is approved to participate in the program through the existing SBA 7(a) lending program and additional lenders approved by the Department of Treasury. There are thousands of banks that already participate in the SBA’s lending programs, including numerous community banks. You do not have to visit any government institution to apply for the program. You can call your bank or find SBA-approved lenders in your area through SBA’s online Lender Match tool.

We hope to have a webinar this week with a panel that would include bankers to provide more details on how to apply/process these loans. Please watch for more information on this.

Income and Payroll Tax Incentives

Several tax incentives have also recently been announced, including:

Quarterly estimated personal tax payments for 2020 – these are payments typically made by owners of S corporations or LLC’s. The first 3 quarterly estimates are due in a lump sum on Oct 15, 2020 (penalty and interest free). These estimates would otherwise be due April 15, June 15 and September 15.

2019 income taxes, income tax returns, and gift tax return due dates have been delayed to July 15, 2020.

Net operating losses incurred in 2018, 2019, or 2020 can be “carried back” up to 5 years to reduce income in a prior year (and obtain refunds). The 30% business interest deduction limit is increased to 50% for 2019 and 2020. The Act also corrects a ‘glitch’ in the 2017 tax act and provides that ‘qualified improvement property’ is eligible for bonus depreciation (and this provision is made retroactive).

Employers may defer deposits of the employer share of social security tax (but not Medicare taxes). The employer social security taxes otherwise due between now and Dec 31 2020 may be deferred as follows: half must be deposited by Dec 31 2021, and the remaining half must be deposited by Dec 31 2022. A similar deferral is available for the social security portion of the employer portion of self-employment tax. It appears that this deferral is not available to those receiving loan forgiveness under PPP.

The Act provides a payroll tax credit against employment taxes owed by eligible employers impacted by COVID-19. An employer is eligible if it: (i) was required by a governmental authority to fully or partially suspended its trade or business during such calendar quarter because of COVID-19 or (ii) experienced a significant decline in gross receipts. An employer generally experiences a significant decline in gross receipts when (i) beginning with the first calendar quarter in 2020 where such employer’s gross receipts are less than 50% of such employer’s gross receipts for the corresponding calendar quarter in 2019 and (ii) ending with the first calendar quarter where such employer’s gross receipts equal 80% of such employer’s gross receipts for the corresponding calendar quarter for the previous year. The payroll tax credit generally equals 50% of the eligible employees’ wages, but the qualified wages per employee may not exceed $10,000. Additionally, an employer receiving a small business interruption loan under PPP is not eligible for this credit.

Families First Coronavirus Response Act

The Families First Coronavirus Response Act (the “FFCRA”) provides sick leave wages and expanded family and medical leave wages for employees impacted by COVID-19. The CARES Act expands the employees eligible for sick leave wages and expanded family and medical leave wages to generally include employees who were laid off on or after March 1, 2020, had worked for the employer for at least 30 of the last 60 calendar days prior to being laid off, and were rehired by the employer.

The CARES Act states that employers who provide sick leave wages or expanded family and medical leave wages can generally obtain an advance of tax credits owed pursuant to the FFCRA. While payroll tax payments are generally due April 30, July 31, October 31, and January 31 each year, the CARES Act provides an extension for payment of certain payroll taxes (discussed above). Therefore, the CARES Act provides employers with the ability to obtain prompt reimbursement of any sick leave wages or expanded family and medical leave wages paid pursuant to the FFCRA.

There is obviously a lot to digest for businesses and business owners, but the above provisions should be carefully evaluated as they are significant. We will keep you posted as developments occur.

March 18th, 2020 5:30PM

Tax Payment/Deadline Extension

Yesterday, March 17, Treasury Secretary Steve Mnuchin announced a 90-day tax payment extension for many individuals and corporations.

Individual taxpayers must still either file their income tax returns or file an extension by April 15, 2020.

Federal income tax payments up to $1 million for individuals and up to $10 million for corporations can be deferred for 90 days, to July 15, 2020, without penalty or interest.

This 90-day deferral applies to amounts due on 2019 income tax returns and 2020 estimated tax payments.

Additionally, many states are offering similar payment extension provisions.

This is an evolving situation, and MST will continue to monitor and communicate information as it becomes available. Please do not hesitate to reach out with any concerns or questions.

March 17th, 2020 12:01PM

We are writing to make you aware of two important matters arising from efforts to deal with the coronavirus outbreak.

1) Yesterday the White House announced additional measures and recommendations designed to minimize exposure to the virus. Toward this end, we are closing our offices to meetings. Implementing “social distancing” within the offices will allow our staff to minimize their potential exposure. We will have staff in the office to receive FedEx and mail, but encourage you take advantage of our secure MST web portal to upload and download documents and deliver electronic signature forms for your personal tax returns. This paperless environment will allow us to continue to serve you at this critical time while limiting contact. Many of our clients are already using our secure portal and email. If you would like to explore using these tools this year, we urge you to contact us at your earliest convenience.

2) Late last week, the President instructed the Treasury and IRS to delay the April 15 income-tax deadline and other tax-related deadlines. No further guidance has been provided by the White House or the IRS at this time. We will continue to monitor the situation and keep you apprised of how it might affect you. However, because the situation is extremely fluid and unpredictable, we urge you to continue working with your MST tax professional to gather all pertinent information we require to process your tax return.

Rest assured that, in these extraordinary times, MST will take all prudent measures to ensure the safety and well-being of our clients and employees, while still delivering the exceptional service you’ve come to expect from us.

Gregory W. Hayes, CPA | Managing Partner